When you fill a prescription for a generic drug, it seems simple: the pharmacy gives you pills, your insurance covers part of it, and you pay the rest. But behind that transaction, there’s a hidden system that rarely gets talked about - and it’s not working the way most people think. Generics make up 90% of all prescriptions filled in the U.S., yet they account for only about 23% of total drug spending. That’s because they don’t work like brand-name drugs when it comes to how insurance pays for them. No big rebates. No complex negotiations. Just a quiet, confusing system that often leaves insurers - and you - paying more than you realize.

Generics Don’t Get Rebates (And That’s the Point)

Most people assume all drugs get rebates. That’s not true. Brand-name drugs? Yes. Generics? Almost never. Why? Because rebates are designed to create competition among manufacturers who charge the same high list price. When multiple companies sell similar brand-name drugs, the one offering the biggest rebate to the pharmacy benefit manager (PBM) gets placed on the insurance plan’s preferred list. That’s how PBMs keep costs down - by playing manufacturers against each other. But generics? There’s no such game. Hundreds of companies make the exact same drug - let’s say lisinopril for high blood pressure. No one has a patent. No one has exclusive rights. The price is set by supply and demand, not by who offers the biggest kickback. So instead of rebates, PBMs negotiate flat prices. That sounds fair, right? But here’s where it gets messy.What Insurance Actually Pays: The Spread Pricing Trap

Here’s the reality: when your insurance pays for a generic, it’s not paying what the pharmacy pays. It’s paying what the PBM says it should pay - and that number is often inflated. How? Through something called spread pricing. Let’s say the pharmacy buys a bottle of generic metformin for $3.50. The PBM tells your insurance plan: "We’ll reimburse you $8.50." So your insurer pays $8.50. But the pharmacy only gets $3.50. The $5 difference? The PBM keeps it. That’s spread pricing. It’s not a rebate. It’s a hidden markup. And it’s completely opaque. Most employers and insurers don’t even know it’s happening until they dig into their claims data. A 2023 analysis by the National Business Group on Health found that 68% of large employers couldn’t accurately determine the true cost of generics because PBMs refused to disclose acquisition prices. One Fortune 500 HR director told Becker’s Hospital Review: "We discovered our PBM was charging us $8.50 per generic prescription while paying pharmacies only $4.25. We were paying $4.25 in hidden fees - every single time."Why This Matters: Generics Are Being Pushed Aside

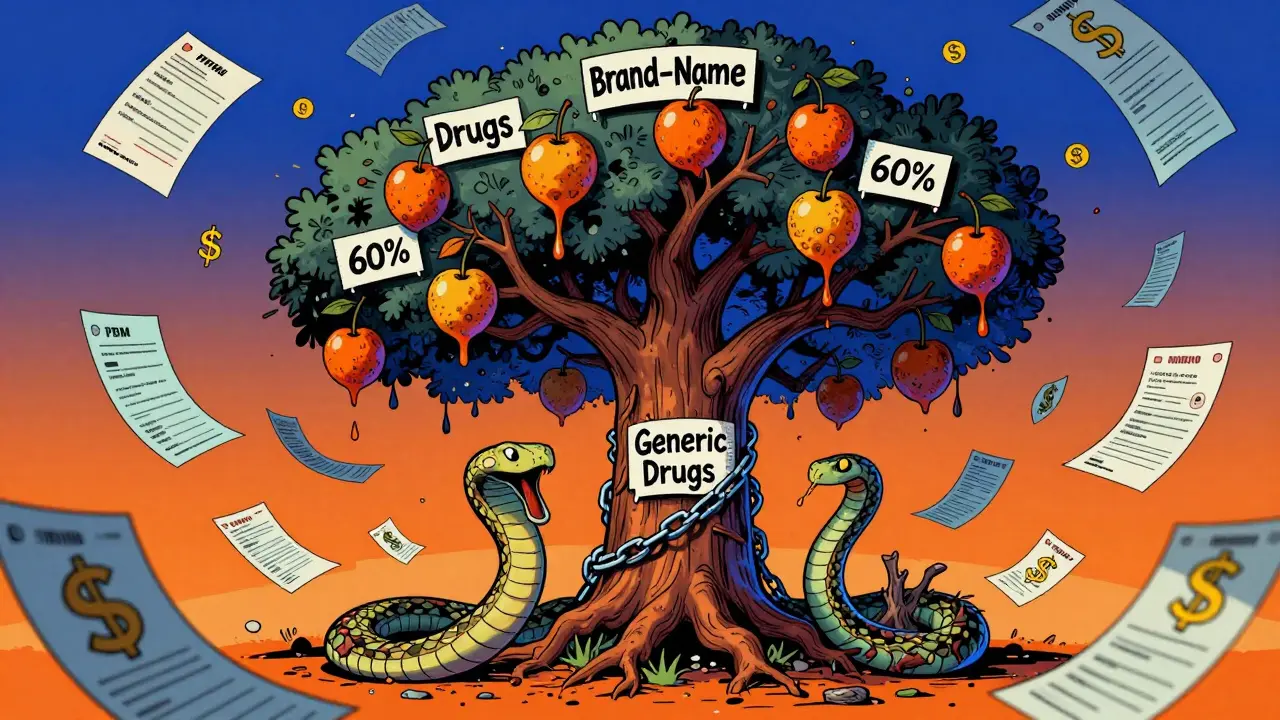

You’d think PBMs would love generics. They’re cheap. They work. But here’s the twist: PBMs make more money from brand-name drugs. Why? Because brand-name manufacturers offer rebates of 30% to 70% of the list price. Generics? Maybe 2% to 5% - if anything at all. So PBMs have an incentive to keep generics off the formulary. Not because they’re bad. Not because they’re unsafe. But because they don’t bring in the same kickback. A 2023 report from Rightway Healthcare found that PBMs sometimes exclude a $0.15-per-dose generic in favor of a $5-per-dose brand-name drug with a 60% rebate. The math? The insurer pays more. The patient pays more. And the PBM pockets the difference. This isn’t hypothetical. In one case documented by the Midwest Manufacturers Association, a PBM blocked a generic version of a heart medication because the brand-name drug offered a higher rebate. The result? Patients paid $200 more per month - even though the generic was chemically identical and FDA-approved.

Who’s Really Paying?

It’s easy to blame insurance companies. But they’re just as confused as you are. Most insurers don’t control their own formularies - PBMs do. And PBMs aren’t required to tell insurers how much they’re keeping from spread pricing. The Department of Labor’s 2024 report found that the average spread on generic prescriptions was $4.73 per fill. Multiply that by 10 billion generic prescriptions a year? That’s nearly $50 billion in hidden fees. And that money isn’t going to drug companies. It’s going to PBMs. Employers who self-insure are the ones who feel this the hardest. They pay the full cost of claims, so every hidden fee hits their bottom line. But even people on fully insured plans aren’t safe. When insurers pay more for drugs, they raise premiums. So you’re paying for it too - through your monthly bill.The System Is Changing - Slowly

There’s growing pressure to fix this. The Biden administration’s 2024 Executive Order directed the Department of Health and Human Services to examine practices that limit generic use. The No Surprises Act of 2020 pushed for more transparency, but it didn’t go far enough. And in March 2025, CMS announced new Medicare drug price negotiations - but guess what? Generics were excluded. Again. Still, change is happening. In 2020, only 18% of large employers used pass-through pricing for generics - where PBMs charge a flat administrative fee and don’t keep the spread. By 2024, that number jumped to 42%. That’s progress. And the Employee Benefit Research Institute predicts that by 2026, federal legislation will require PBMs to disclose the true acquisition cost of every generic drug.

What You Can Do

If you’re an employer or plan sponsor, demand transparency. Ask your PBM: "What do you pay pharmacies for the top 10 generics we use?" If they won’t tell you, it’s time to switch. If you’re a patient, check your copay. If your generic costs more than $10 at the pharmacy, ask your doctor if there’s a cheaper alternative - and whether your plan has a preferred pharmacy. Sometimes, mail-order or specialty pharmacies offer better prices. And if you’re confused? You’re not alone. The system is designed to be confusing. But the truth is simple: generics should be the cheapest option. Right now, they’re not. And that’s not because of the drugs. It’s because of the middlemen.Do generic drugs have rebates like brand-name drugs?

Generally, no. Generic drugs rarely have rebates because they’re already priced competitively by multiple manufacturers. Unlike brand-name drugs, where companies offer 30-70% rebates to get on formularies, generics operate on flat pricing. Any rebate offered is usually under 5% - if at all.

Why do insurers pay more for generics than pharmacies charge?

Because of spread pricing. Pharmacy benefit managers (PBMs) set a reimbursement rate to insurers that’s higher than what they actually pay pharmacies. The difference - often $4 to $5 per prescription - is kept by the PBM as profit. This isn’t disclosed in most insurance contracts.

Can PBMs block generic drugs from insurance plans?

Yes. PBMs sometimes exclude low-cost generics to favor higher-priced brand-name drugs that offer bigger rebates. This creates a perverse incentive: the cheapest drug isn’t always the one covered. In some cases, patients have to appeal or pay out-of-pocket to get a generic they need.

How much do PBMs make from generic drug spread pricing?

The average spread on generic prescriptions is $4.73 per fill, according to the U.S. Department of Labor (2024). With over 10 billion generic prescriptions filled annually in the U.S., that adds up to nearly $50 billion in hidden fees going to PBMs each year.

Are generics excluded from Medicare drug price negotiations?

Yes. The Inflation Reduction Act of 2022 explicitly excludes generic drugs and biosimilars from Medicare’s drug price negotiation program. The law assumes competition among manufacturers keeps generic prices low - but it doesn’t account for hidden PBM fees that inflate what insurers and patients actually pay.

What’s the difference between WAC, AWP, and net price for generics?

Wholesale Acquisition Cost (WAC) is what manufacturers charge pharmacies. Average Wholesale Price (AWP) is an outdated list price used as a billing benchmark - often inflated. Net price is what the insurer actually pays after any discounts or rebates. For generics, net price is usually close to WAC - but spread pricing makes it look like the insurer paid much more.

Rosemary Chude-Sokei

March 14, 2026 AT 21:16It’s wild how little most people know about how PBMs operate. I work in healthcare administration, and even I was shocked when I first saw the spread pricing numbers. It’s not just unethical-it’s systemic. The whole structure incentivizes complexity over transparency, and patients are the ones who pay the price, literally and figuratively.

Generics should be the backbone of affordable care, not a profit center for middlemen. The fact that CMS excludes them from price negotiations is baffling. If anything, they’re the ones that need oversight the most, because there’s no patent protection to keep prices low-just market forces, which PBMs have corrupted.

Employers need to demand full disclosure. Pass-through pricing isn’t a luxury; it’s a necessity. And if PBMs refuse? Fire them. No more excuses.

Ali Hughey

March 15, 2026 AT 08:29THIS IS A SCAM. A FULL-ON, BIG PHARMA + PBM CONSPIRACY. 🤯

They don’t want you to know this. They don’t want YOU to know this. Why? Because if you knew, you’d riot. 😱

Generics are CHEAPER. They’re FDA-approved. They work. But PBMs? They’re literally stealing $5 per prescription and calling it ‘administrative fees.’ 😭

And guess what? The government’s SILENT. Because they’re in bed with them. 💼🩺

Next time you pay $15 for lisinopril… ask yourself: who’s REALLY getting rich? Not the pharmacist. Not the manufacturer. The middleman. The puppet master. The PBM. 🕵️♂️💸

Alex MC

March 16, 2026 AT 23:56Interesting breakdown. I’ve always assumed generics were straightforward, but this makes sense in a twisted way.

The PBM model is like a black box-everyone’s paying, no one knows how much, and nobody’s accountable. It’s frustrating, but not surprising.

I’m glad to see more employers pushing for pass-through pricing. It’s a small step, but it’s a step. Maybe if enough people ask the right questions, the system will have to change.

Also, props to the author for not just complaining but giving actionable steps. That’s rare these days.

rakesh sabharwal

March 17, 2026 AT 21:29The entire pharmaceutical supply chain is a grotesque manifestation of neoliberal rent-seeking. PBMs, as non-regulated intermediaries, function as extractive monopolies-leveraging information asymmetry to siphon surplus value from both payers and providers.

Spread pricing is not merely a pricing mechanism; it is a structural artifact of deregulated healthcare capitalism. The exclusion of generics from Medicare negotiation is not an oversight-it is a deliberate policy choice to preserve the rentier class.

One must question the epistemological foundations of ‘market competition’ when the market is artificially distorted by opaque rebates and non-disclosure clauses. The solution? Public utility regulation of PBMs. Full stop.

Aaron Leib

March 18, 2026 AT 12:04Good post. Real talk: if you’re an employer, ask your PBM for the acquisition cost. If they hesitate? Walk away.

It’s not about being angry. It’s about being smart. The math doesn’t lie.

And patients? You’re not powerless. Ask your pharmacist. Ask your doctor. Ask your HR. Just ask.

Small steps. Big impact.

Amisha Patel

March 19, 2026 AT 06:43I never realized PBMs could block generics just because they don’t offer rebates. That’s wild. So the cheapest option isn’t always covered? That feels backwards.

Does this happen in India too? I know our drug prices are low, but I wonder if similar middlemen exist there.

Thanks for explaining this so clearly. I’m going to ask my employer about this next time we review benefits.

Elsa Rodriguez

March 19, 2026 AT 15:56Ugh. I knew something was off with my $12 generic copay. I thought I was getting ripped off by the pharmacy. Turns out, the insurance company is being robbed… and I’m still paying for it.

This is why I hate healthcare. It’s all smoke and mirrors. And the people who *really* get rich? They’re not even in the room.

Also-why is no one in Congress doing anything? Are they all on PBMs’ payroll? 😒

So. Much. Anger.

Serena Petrie

March 21, 2026 AT 07:45They’re not even trying to hide it anymore.

Buddy Nataatmadja

March 21, 2026 AT 07:47Interesting how this mirrors other industries-like airline ticketing or hotel booking. The middleman makes money off the gap, not the service.

Kinda makes you wonder what else we’re paying for without knowing it.

Also, I didn’t know about the Medicare exclusion. That’s… concerning.

mir yasir

March 22, 2026 AT 06:19The structural inefficiencies inherent in the American pharmaceutical distribution model are a textbook case of regulatory capture. PBMs, as third-party administrators, operate under a fiduciary void, wherein their contractual obligations to insurers are fundamentally misaligned with patient welfare.

The phenomenon of spread pricing constitutes a latent tax on healthcare access, disproportionately affecting self-insured employers and low-income populations.

One must conclude that the current regulatory framework is not merely inadequate-it is complicit.

tynece roberts

March 24, 2026 AT 05:49so like… the pharmacy gets $3.50, insurance pays $8.50, and the pbs just… keeps the $5? like??

that’s not even a business model. that’s just stealing.

and they say generics are cheap? no. they’re just *hidden* expensive. i hate this. i really do.

my dad’s on lisinopril. he pays $15. he’s 72. he shouldn’t have to. why is this allowed? 😭

also i think i just found my new hobby: digging into my insurance statements.

Hugh Breen

March 24, 2026 AT 06:18Wow. Just… wow. 🙏

This is the kind of post that makes you realize how much you don’t know-and how much needs to change.

Thank you for breaking this down. Seriously.

And hey-if you’re reading this and you’re an employer? Don’t wait. Ask your PBM. Now.

If we don’t push for transparency, who will?

✊ #HealthcareTransparency